The pre-completed tax return – making corrections in MyTax or on paper

In March or April, you will receive your pre-completed tax return in MyTax and by post. If you have activated Suomi.fi messages, you will receive an email when the tax return is ready for viewing in MyTax.

See the planned schedule for tax returns

Check your tax return and make the necessary corrections and additions. If all the information is correct, you do not need to do anything.

These instructions follow the order of the tax return’s sections in MyTax. It is not entirely the same order as on the paper version. However, the text below covers all the sub-headings and sections of the paper form.

Please note that the MyTax view does not contain numbered enclosure forms (such as Form 7H Rental income – Apartments in a housing company, or other numbered forms). Instead of having to fill in many numbered forms for different kinds of income, you simply enter the amounts under the appropriate sections in MyTax. There is a specific section for rental income, for example.

-

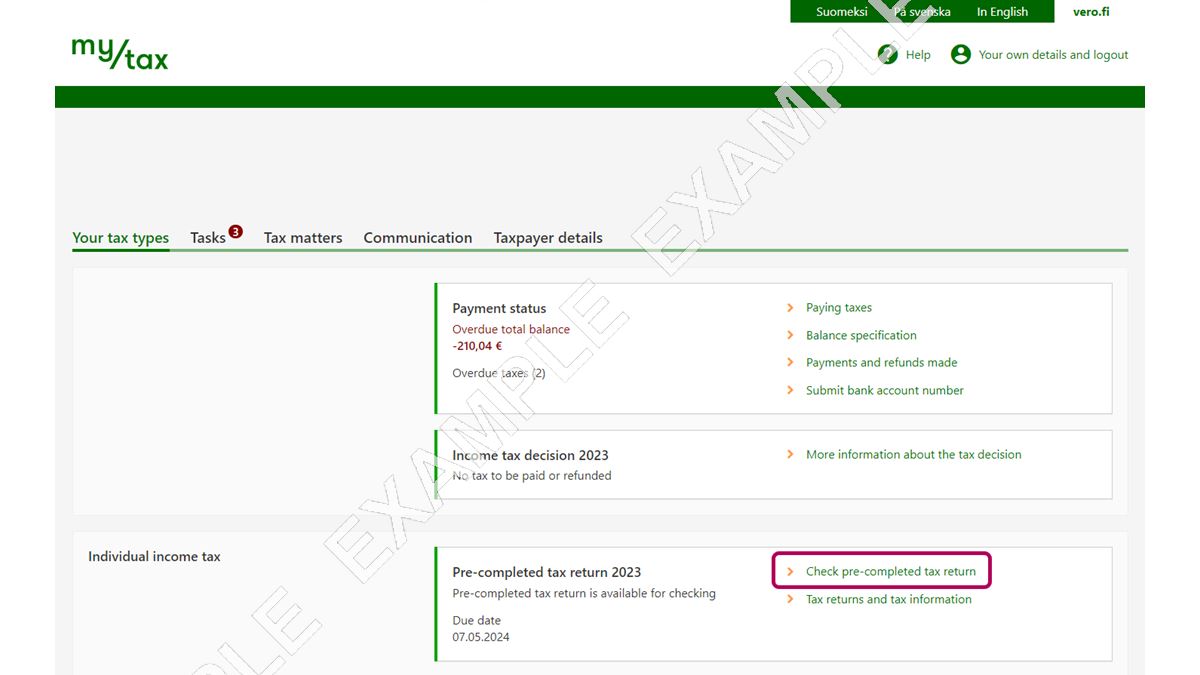

First, go to the Individual income tax section and select Pre-completed tax return 2023, then click the link Check your pre-completed tax return.

-

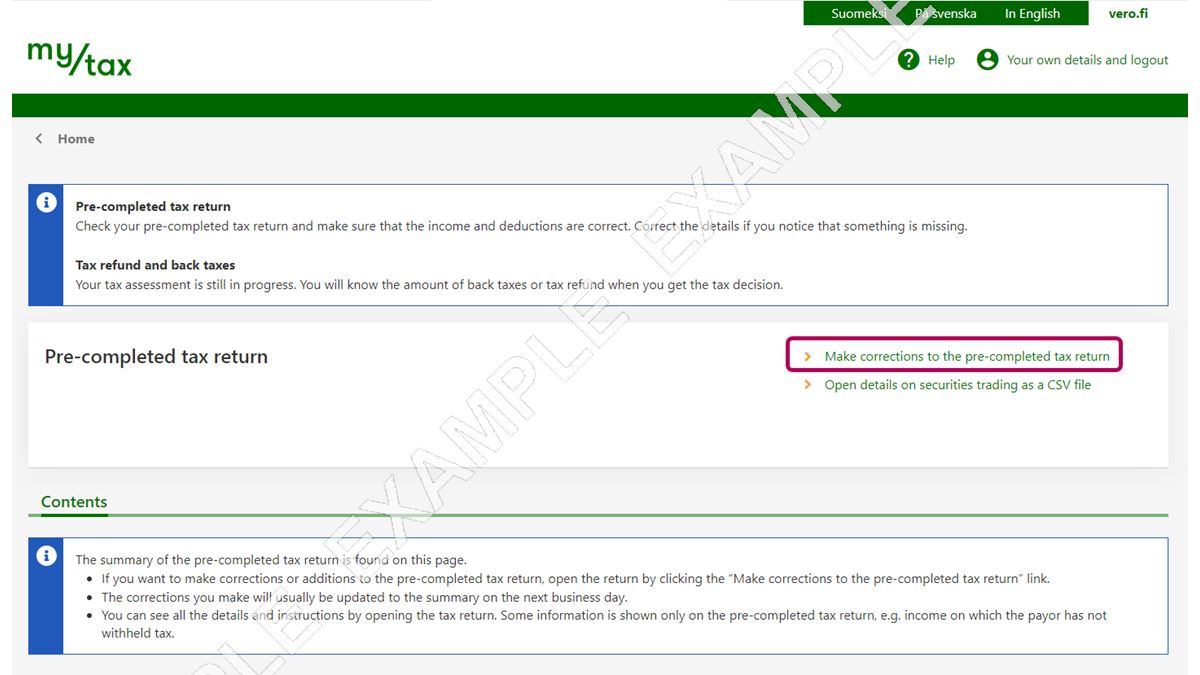

Click Make corrections to the pre-completed tax return.

Here you can also find the link Open details on securities trading as a CSV file. If you have sold stocks or other securities during the tax year, you can view the trading in table format. Please note that you cannot edit or send data via the table. Make changes in the Profit from selling securities section on the tax return.

-

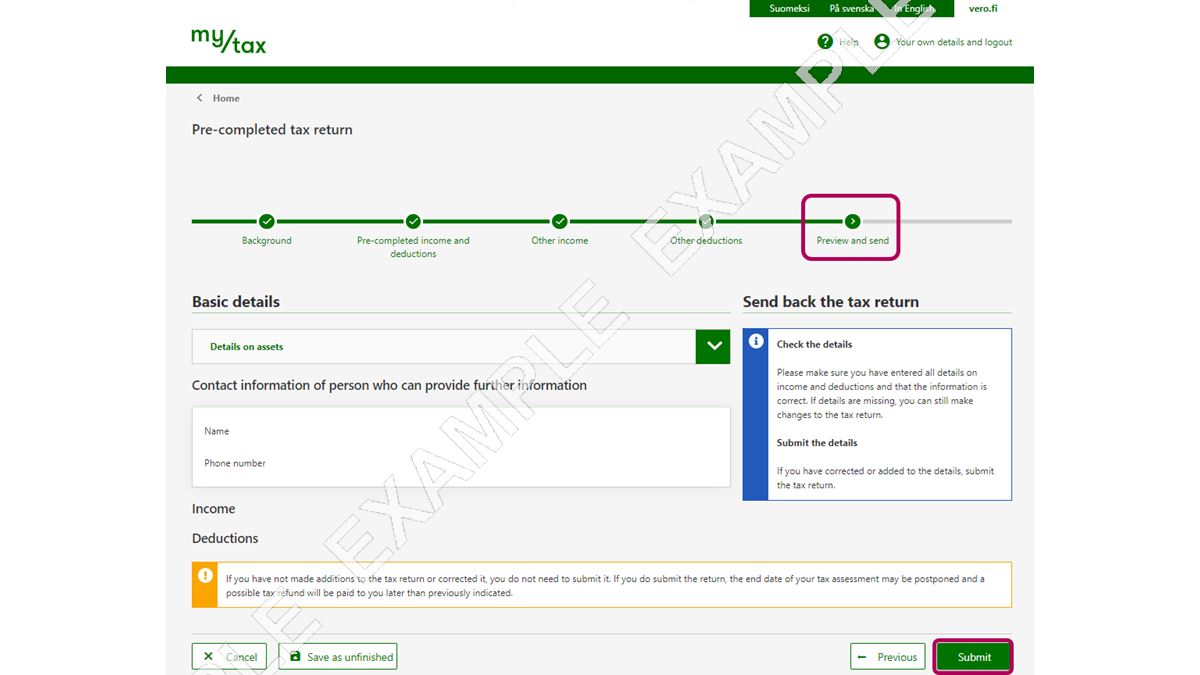

The tax return has 5 stages. If you make changes to your tax return, you can send it at Preview and send, which is the last stage of the tax return. Scroll down the page and click Submit.

{kind=link}

{kind=link}

This section contains the following personal information as applicable to you:

- name

- bank account number in the Tax Administration records

- municipality of domicile

- parish (basis for church tax)

- spouse

- number of underage children

- disability percentage if you are an Åland-domiciled individual taxpayer.

The Tax Administration receives most of the above information (name, municipality of domicile, etc.) from the Population Information System. If it is necessary to make corrections to the above information, you can contact the DVV to request that any errors are put right.

- The municipality of domicile is the municipality where you lived on the last day of the year before the tax year.

- Membership in a church parish is also determined by the records valid on the last day of the year before the tax year. Read more about church tax (in Finnish and Swedish, link to Finnish).

- If there is a mistake regarding your home address, refer to the instructions on making a change of address.

- If your municipality of domicile is on Åland and the 2023 tax year is the first time when you claim a deduction due to disability, please submit Form 17 – Ålandsbilaga and give details on your disability, enclosing a medical certificate or other documentation concerning the degree/percentage of disability. Unfortunately, MyTax cannot be used for submitting this information. Note: from tax year 2023, no deduction for disability is available for people who live in mainland Finland.

- In general, if you get married or divorced, it is not necessary to inform the Tax Administration of it. Read more about the differences in tax treatment that depend on family relationships.

How to file in MyTax

In the Basic details section, you can inform the Tax Administration if you have separated from your spouse during the tax year.

How to file on paper

To inform the Tax Administration that you have separated from your spouse, you can submit Form 50A (Earned income and deductions)

If your bank account number is wrong or missing, submit the correct account number. MyTax shows the bank account number in the international IBAN format.

- See the instructions: How to submit a bank account number in MyTax

- See the instructions: Notifying the bank account number of an estate of a deceased person

MyTax also allows you to submit the bank account number of your underage child. Children under 18 can also submit their own bank account numbers in MyTax if they have personal online banking codes or a mobile certificate.

This section contains the following details on assets:

- apartments, i.e. shares in housing companies and mutual real estate holding companies

- shares in other companies and cooperatives (not customary shares in consumer cooperatives and cooperative banks)

- real estate property

- shares in investment funds and UCITS

- other securities and book-entry shares (not bonds or debentures subject to tax at source on interest income or corresponding bonds or debentures within the EEA)

- equity savings account

- shares in general partnerships, limited partnerships and other partnerships

- rights of possession or rights of use to a real estate unit, to shares in housing or real estate companies or to other securities

- assets and property located outside Finland.

Do not report other assets, such as cars, boats or household effects.

To check the full details on the real estate units you own, see the real estate tax return. If you have bought, acquired, sold or otherwise transferred a real estate unit, or if repairs or changes have been made to a real estate unit you own, report the details on your real estate tax return.

The tax return shows the assets that were in the Tax Administration records on 31 December 2023. If the details on assets contain errors or if an item of property is not shown, please make corrections as appropriate. Also report the changes to your assets that have taken place during the tax year.

How to file in MyTax

The assets on record are listed in the first part of the tax return, i.e. in the Background information stage.

- If only some of your assets and property are shown under Details on assets, click the Add a new asset button to add the missing details.

- If previous sales and other transfers are incorrectly shown as assets, make a correction by clicking the Add a new asset button.

- Select the asset type, enter 0% as the share of ownership and type the details on the incorrectly shown asset in the description field.

- If you are making corrections to details concerning shares in a housing company, you can add the deed of sale as an attachment.

- If you have sold or otherwise transferred your assets, report the details on the transfers later in their own sections (Capital gains or Profits from selling securities).

How to file on paper

Select a correct form:

- To make corrections to the details on assets, fill in Form 50B Capital income and deductions. Report the changes in section 6 Changes to assets.

- To report transfers of securities, fill in Form 9A – Capital gains and capital losses from trading with securities.

- For sales and transfers of other property, submit Form 9 – Capital gain or capital loss.

Income

Pay, fees and pensions

This section contains the following details:

- Wages, salaries, fees and compensation:

- wages

- fringe benefits

- fees and compensation received in private or public sector employment

- employee stock options and stock grants

- taxable reimbursement of expenses

- reimbursements of a daycare provider's expenses

- staff loan interest benefit regarded as wages

- insurance premiums regarded as wages

- Trade income and compensation for use:

- trade income received by a person who is VAT liable

- trade income received by a person who is not VAT liable

- compensation for use, royalties and compensation for employee invention

- Foster care provider’s or family caregiver’s fees

- Dividends and surplus based on work effort, treated as trade income or wages

- Income from seafaring (wages and fringe benefits)

- Other earned income:

- sportsperson’s and athlete's fees

- other taxable income subject to withholding including receipts of grants to support a recreational activity and miscellaneous fees received

- occasionally

- personnel fund units and surplus

- supplementary daily allowance from a health insurance fund

- expense reimbursement paid to conciliator

- Wages paid by a foreign employer:

- wages received from a foreign employer that does not have a permanent establishment in Finland

- wages from a foreign employer based on a net-of-tax contract or seafarer's income from a foreign employer

- foreign wage income and seafarer's income subject to health insurance contribution only

- employee stock options and stock grants based on foreign wages and seafarer's income.

The employer or other payor submits reports to the Incomes Register on all the wages it pays out. The Tax Administration receives the payroll information from the Incomes Register and transfers it to your pre-completed tax return.

If there are errors in the amounts or if something is missing, make the necessary corrections and inform your employer/payor of the errors so that they can submit the corrections to the Incomes Register.

If you worked outside of Finland, indicate the amount of your pay in the Foreign income section.

If you claim reduction in the value of a car benefit, see the guidance in section Reduction in the value of a company car benefit.

Using MyTax to make corrections or to add information

A) Select the link with the payor's name.

If the payor’s name is not on the list, see instructions under section B.

- If the amount of income is incorrect, enter the correct amount to replace it.

- If you have not received the income, click the Delete button.

- If you add a new item of income from the same payor, click the Add income button. Report the details on the income and the amounts withheld on the income.

- Click the Add a deducted contribution button, if any of the following deductions is connected to the income:

- mandatory pension insurance contributions

- mandatory unemployment insurance contributions

- reimbursements of foster care provider’s expenses

- contributions for collective additional pension insurance

Click OK to finish.

B) Click the Add new payor button.

- Fill in the payor’s Business ID or personal identity code, and the payor’s name.

- Click the Add income button. Report the details on the income and the amounts withheld on the income.

- Click the Add a deducted contribution button, if any of the following deductions is connected to the income:

- mandatory pension insurance contributions

- mandatory unemployment insurance contributions

- reimbursements of foster care provider’s expenses

- contributions for collective additional pension insurance

Click OK to finish.

If you have received income from different payors, add the income items from every payor separately. To do this, click Add new payor as many times as necessary.

Further information

How to file on paper

If you file or correct your wage details on a paper form, submit Form 50A – Earned income and deductions.

The payor-reported social benefits in this section include:

- earnings-related unemployment allowance

- basic daily allowance

- labour market subsidy

- maternity allowance, parental allowance

- paternity allowance (estimated due date of your baby was before 4 September 2022)

- allowance for child home care

- study grant

- sickness allowance

- adult education allowance

- allowance for communicable diseases.

Kela and other payors of benefits report the data to the Incomes Register. The Tax Administration receives the information from the Incomes Register and transfers it to your pre-completed tax return. Check the details and make corrections if needed. If you notice any errors, you should also inform the payor of the errors, so they can submit corrections to the Incomes Register.

This section is not for reporting any benefits that you may have received from payors outside of Finland. Enter benefits from abroad separately in the Foreign income section.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of various benefits.

If corrections are necessary or if you need to add a new benefit from the same payor, do as follows:

- Under Benefits and pensions in 2023, click the link with the payor's name.

- Click the Edit details button. If necessary, you can also delete incorrect benefit information by clicking the Delete information button.

- If benefits paid by the same payor are missing, click the Add benefit button.

If you need to add a new benefit from a new payor, click the Add a payor button.

If no benefits income is pre-completed, please move on to the Other income stage. Select Yes for “Benefits and pensions treated as earned income, reported to the Incomes Register by the payor”. Then click Add a payor.

-

First select the payor (Kela, Keva or Other Finnish payor).

-

If you selected Other Finnish payor and you cannot find the name of the payor on the list, please scroll to the Other Finnish payor section, select it and then enter the name of the payor in the field that appears.

-

Click Add a benefit, fill in the benefit’s type/amount, and click OK.

-

If you need to give details on still other social benefits, click Add a benefit again.

-

Then scroll down to Withholdings from the income received from the payor to fill in the total amount that your payor(s) withheld when paying you these benefits.

How to file on paper

If you report or correct benefit information on paper, submit Form 50A – Earned income and deductions.

This section contains your pension income from Finnish sources:

- earnings-related pensions and pensions for the self-employed

- pension in accordance with the National Pensions Act

- guarantee pension

- pension based on insurance and taxed as earned income

- pensions you receive as a non-resident taxpayer.

The payor of the pensions reports the data to the Incomes Register. The Tax Administration receives the information from the Incomes Register and transfers it to your pre-completed tax return. Check the details and make corrections if needed. If you notice any errors, you should also inform the payor, so they can submit corrections to the Incomes Register.

If you have received pension from abroad, check or fill in the details under Foreign income.

You can ask for tax periodisation of a pension if it was paid to you retroactively

If you were paid a lump sum of a statutory pension in a retroactive way, you can demand tax treatment based on periodisation of the pension income, i.e. that the income be allocated for a previous year. You can do so if you received retroactive pension, for at least 3 months connected to a previous year, and if the amount was at least €500.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of pensions.

If corrections are necessary or if you need to add a new pension from the same payor, do as follows:

- Under Benefits and pensions in 2023, click the link with the payor's name.

- Click the Edit details button.

- By clicking the Edit details button, you can also request the periodisation of retroactive pension. Answer Yes to the question “Do you request periodisation of pension income?” and then fill in the required details. You can also submit details on the periodised pensions as an attachment.

- If pensions paid by the same payor are missing, click Add a pension.

If you need to add a new pension from a new payor, click Add a payor and enter the required details.

If none of the above pensions are pre-completed, please move on to the Other income stage.

- First click Yes in the Pensions and benefits treated as earned income, reported to the Incomes Register by the payor, and then click the Add a payor button.

- Click the Add a pension button under Pensions. Fill in the amounts and other data, then click OK.

- Scroll down to Withholdings from the income received from the payor and enter the total amount of tax withheld.

Non-resident’s pensions

If you live in a foreign country and you are a non-resident taxpayer, you can see your pensions under Non-resident’s pensions.

- You can see the information by clicking the Edit details button.

- By clicking the Edit details button, you can also request the periodisation of retroactive pension. Answer Yes to the question “Do you request periodisation of pension income?” and then fill in the required details. You can also submit details on the periodised pensions as an attachment.

- If pensions paid by the same payor are missing, click the Add a pension button.

- If you need to add a new pension from a new payor, click Add a payor and enter the required details.

Pension income and taxes paid abroad (reverse credit)

According to certain tax treaties, double taxation is eliminated exceptionally in the country from which the income is received. Tax paid on Finnish pension to a foreign country of residence can be credited if

- you live in Spain and receive pension from Finland. Read more: You live in Spain and receive pension from Finland

- you live in Switzerland, Thailand or Italy and have received a pension from Finland based on Finnish social security legislation.

If you live in one of these countries and have paid taxes to your country of residence from income you received from Finland, you can claim credit for taxes paid abroad. In this case, select Yes in the section Taxes paid abroad and enter the amount of tax.

How to file on paper

If you file or correct your pension details on paper, submit Form 50A – Earned income and deductions.

Further information

- Read more about the taxation of pension income (detailed guidance) (in Finnish and Swedish, link to Finnish)

- Read more about Taxation of pension income in cross-border circumstances (detailed guidance)

- Read more about non-residency (detailed guidance)

This section contains the following:

- pension, benefits and taxable life annuity paid by a natural person and an estate

- payment based on a long-term savings contract, taxed as earned income

- payment based on a long-term savings contract, taxed as capital income and raised by 20% or 50%

- annual capital income payment based on a long-term savings contract

- assets saved under a long-term savings contract and paid out in circumstances where the owner or another person entitled to the assets has died.

The Tax Administration receives information on paid-out pensions and the taxes withheld on the amounts directly from the payors. Accordingly, the pre-completed tax return often contains details on the pensions.

Enter pensions you have received from abroad separately in the section Foreign income.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of pensions.

If you wish to make corrections, click Edit and enter the amount of pension and the amount withheld.

If a pension or a payment you have received based on a long-term savings contract is missing, click Add new pension and fill in the missing details.

If no income in the form of pensions is pre-completed, please move on to the Other income stage. First click Yes in Received pension based on a long-term savings contract, and then click the Add new pension button.

Further information

- Read more about the taxation of long-term savings contracts (detailed guidance) (in Finnish and Swedish, link to Finnish)

How to file on paper

If you file or correct pension information on paper, submit Form 50A – Earned income and deductions.

This section contains the following:

- taxable strike pay

- repayment of statutory pension insurance premiums

The Tax Administration receives information on paid-out strike pay and repayments of pension insurance premiums as well as on the taxes withheld on the amounts. These details are usually available on the pre-completed tax return.

How to file in MyTax

The Pre-completed income and deductions stage contains the information on strike pay and repayments of pension insurance premiums that has been available to the Tax Administration. If you wish to make corrections, click Edit and enter the benefit amount and the amount withheld.

If some of the payments you have received are missing, click Add new benefit and enter the required details.

If no income in the form of benefits is pre-completed, please move on to the Other income stage. First click Yes in Other benefits, and then click the Add new benefit button.

How to file on paper

If you file or correct benefits information on paper, submit Form 50A – Earned income and deductions. Report this information in section 5 Benefits.

Capital income

This section contains the following:

- the returns derived from insurance contracts subject to special tax treatment (§ 35b of the act on income tax)

- profit from a capital redemption policy

- other pensions and benefits taxable as capital income

- pensions based on voluntary pension insurance.

The payor of the pensions reports the data to the Incomes Register. The Tax Administration receives the information from the Incomes Register and transfers it to your pre-completed tax return. Check the details and make corrections if needed. If you notice any errors, you should also inform the payor, so they can submit corrections to the Incomes Register.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of pensions that are treated as capital income.

If corrections are necessary or if you need to add a new pension from the same payor, do as follows:

- Under Pensions in 2023, click the link with the payor's name.

- Click the Edit details button.

- If pensions paid by the same payor are missing, click the Add a pension button.

If you need to add a new pension from a new payor, click Add a payor and enter the required details.

If no pension income as described above is pre-completed, go to the Other income stage. Select Yes in the section “Pensions treated as capital income, reported to the Incomes Register by the payor” and then click Add a payor.

- Select the name of the payor from the drop-down menu and click Add a pension.

- If you cannot find the name of the payor on the list, scroll down the menu to the section Other Finnish payor, select it and then enter the name of the payor in the field that appears.

- First click Add a pension and then fill in the pension’s type and amount. Click OK.

- Scroll down to Withholdings from the income received from the payor and enter the total amount of tax withheld.

Non-resident’s pensions

If you live in a foreign country and you are a non-resident taxpayer, you can see your pensions under Non-resident’s pensions. If corrections are necessary or if you need to add a new pension from the same payor, do as follows:

- Select the link with the payor's name.

- Click the Edit details button.

If pensions paid by the same payor are missing, click the Add a pension button.

If you need to add a new pension from a new payor, click Add a payor and enter the required details.

If no pension income is pre-completed, go to the Other income stage. Select Yes in the section Pensions treated as capital income, reported to the Incomes Register by the payor and then click Add a payor.

- Select the name of the payor from the drop-down menu and click Add a pension.

- If you cannot find the name of the payor on the list, scroll down the menu to the section Other Finnish payor, select it and then enter the name of the payor in the field that appears.

- Click Add a pension paid to a non-resident and enter the type and amount of the pension. Click OK.

- Scroll down to Withholdings from the income received from the payor and enter the total amount of tax withheld.

How to file on paper

If you file or correct the above details on paper, submit Form 50B – Capital income and deductions. Report pensions treated as capital income in section 3 of the form.

This section contains the following amounts of income:

- Compensation for use that you have received in exchange for use of a copyright or industrial property right that you have inherited or bought (royalty). Copyright royalties may be related to a literary work, a work of art, or a photograph. Industrial property rights include patents, design rights and trademarks.

- Capital income paid to you by your employer, e.g. guarantee commissions and interest on wage receivables.

Any information on other kinds of compensation for use must be reported under Compensation for use and compensation for employee invention.

Payors of copyright royalties and the employers that have paid capital income to a worker must submit reports on these amounts to the Incomes Register. The Tax Administration receives the information from the Incomes Register and transfers it to your pre-completed tax return. Check the details and make corrections if needed. If you notice any errors, you should also inform the payor, so they can submit corrections to the Incomes Register.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of compensation for use and capital income paid by your employer.

- To make corrections, select the link with the payor's name and edit the details. If only some of the income is shown, select Add income to fill in the missing details.

- If any payor’s information is not pre-completed, click Add new payor to enter the relevant information.

If no income as described above is pre-completed, go to the Other income stage. Select Yes for Compensation for use capital income and capital income paid by employer. Then click Add new payor.

- Fill in the payor’s information and click the Add income button.

- Enter the type of the income and the amount. Also enter the amount withheld from the income.

How to file on paper

If you file or correct the above income information on paper, submit Form 50B – Capital income and deductions. Report this type of income as other capital income under the paper form’s section 3.

This section is for the rental income you have received for offering e.g. the following types of assets for rent:

- apartment(s) in a housing company

- real estate property

- timeshares related to vacation homes

- cars, caravans, boats

- machinery or equipment

It is necessary to report the details on your rental operations although it might be that your rental income has been low, and after the related deductible expenses, you have little or no income subject to tax. The related expenses can also be claimed here. See a list of expenses that can be deducted from rental income.

If you own only a certain part of the rental property, you should report income reflecting the size of the part that you own. Fill in your part of the rental income, and only your share of the deductible expenses related to the rental operation.

If you have previously informed the Tax Administration of your rental income when requesting a tax card or when completing another tax return or if you have paid rental-related prepayments, there may be a pre-filled amount on your tax return. Check all the entries, and if anything is missing, make corrections as appropriate.

Note: Any rental income you have had from a source outside Finland must be reported under the Foreign income section. Information on any rental income relating to an agricultural farm must be reported on the tax return for agriculture. This income includes the rental income you may receive from renting out a field.

Did you use a platform, an app, a website to rent out property to guests and tenants? The Tax Administration receives information concerning the income paid to you through digital platforms both in Finland and abroad. The Tax Administration requires that you report all this income, and we monitor data streams to check for discrepancies. Remember to fill in the tax return giving details on your income and related expenses, because these may be missing from the pre-completed tax return.

How to file in MyTax

The Pre-completed income and deductions stage contains the information made available to the Tax Administration on your rental income. If you make corrections, select the link for the rented-out property. Edit the necessary details.

If only some of the rental income is shown, add the missing income by clicking the Add new rental income button.

If no rental income is pre-completed, got to the Other income stage. Select Yes in the Rental income section and click the Add new rental income link.

- Select the type of property and assets you have rented out.

- Enter more detailed information on an apartment, for example. Note that you can only report the details of one apartment at a time.

- Report all the tenants who have rented this property during the year.

- Enter the rental income and expenses of this particular property in their respective fields.

- Click OK.

If you have received rental income from other sources as well, click Add new rental income again.

If you make depreciations on the acquisition costs for buildings, furniture, appliances and other movable property, report the information in the Calculation of depreciation section, which is visible in MyTax only in case your rental property is real estate or other rental property. Read more about depreciation expenses

Further information

How to file on paper

Select a correct form:

This section contains information on the sales and other transfers of property, including:

- shares that entitle to own an apartment in a housing company or in a real estate holding company

- real estate such as a house, a plot of land or a farm

- capital gains from virtual currencies, such as bitcoin (enter the profits from the mining of virtual currency at Other earned income).

- corporate stock in a non-listed company (not traded at a stock exchange)

- shares relating to a business partnership, such as a general partnership or a limited partnership

- fixed assets i.e. machinery that you have used in a forestry operation.

Note: Your capital gains and capital losses from trading with securities are shown in their own section. Go to the Foreign income section to report details on any selling and transfer of property located in foreign countries.

The capital gains and losses that have resulted from your selling of real estate, housing-company shares and other property are pre-filled on your pre-completed tax return. These gains and losses have been calculated by the Tax Administration and they are based on the information that has been available. Check all the entries, and if anything is missing, make corrections as appropriate.

Report all transfers of property even if the gains were not taxable income or if the losses were not deductible. For example, selling your home is exempted from tax, and in the same way, if property has changed hands under the tax rules on passing a farm or business on to certain close relatives, the transfer is exempted. Although the transactions described above were tax-exempt when they were made, you are still expected to report them.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your transfers of property. If you make corrections, select the link for the rented-out property/asset. Edit the necessary details. If only some of the transfers are showing, click the Add a new transfer button to fill in the details that are missing.

If no details on transfers are pre-completed, go to the Other income stage. Select Yes in the Capital gains and losses section, and then click Add new transfer.

First select the type of property you have transferred:

- shares in a housing company or real estate company

- real estate such as a house or a plot of land

- virtual currencies

- other property including timeshares, shares of a golf course company, or selling of shares in a non-listed company.

Then fill in the required details. Scroll down the bar on the right to see all the sections.

In the case of virtual currencies, see the instructions: How to report gains and losses from virtual currencies in MyTax.

If you had co-owned the sold property together with someone else,

- You must only enter a selling price that reflects your co-ownership (do not enter the full selling price that was received).

- In the same way, when you fill in the other fields, enter your portions only, in proportion to the part you had co-owned, of the property’s acquisition cost, and of the property’s selling expenses.

- If you have sold property together with your spouse, for example, it is important that they submit their own report to the Tax Administration to give details on the sale.

- If you have sold all of the co-owned property’s portion that belonged to you, answer Yes to “Have you sold the entire apartment?”.

- If you did not sell your personal portion entirely, answer No. Enter the sold part as a fraction or as a percentage. For example, if you sold half of the part that you owned, you can enter 50% or ½.

If the sales transaction is tax-exempt because it consisted of selling your home,

- Answer Yes to “Was the sold apartment your own permanent home?”

- Then fill in the required details.

- Finally, click OK.

Further information

- Read more about selling residential property.

- Read more about the taxation of virtual currency

- Calculate the gain or loss from virtual currencies with a calculator (available in Finnish and Swedish, link to Finnish)

How to file on paper

- Use Form 9 Capital gain or capital loss to report your gains and losses from sources in Finland.

- Use Form 16B Statement on foreign income (capital income) to report your gains and losses related to selling, transfers etc. of property located in a foreign country.

This section is for the capital gains and losses related to the following categories of assets and property:

- corporate shares and securities of other types, including those that you sold through the services of a foreign remote intermediary

- shares in investment funds

- refunds of corporate capital to shareholders, when the refund it treated as a transfer of property for tax purposes and when a non-listed company paid the refund.

In addition, sales or redemption transactions relating to bonds or debentures can result in taxable capital gains or tax-deductible capital losses.

The Tax Administration usually receives the information on sales of securities and fund shares from banks, other intermediaries and investment fund companies in Finland and other countries. Check the information and make additions as necessary.

If the acquisition date and acquisition price are missing

The pre-completed tax return may be missing the acquisition date and the acquisition price of a security, for example. In this case, to calculate the taxable capital gain, we apply a deemed acquisition cost, which is either 20% or 40% of the selling price of the shares.

The capital gain is calculated with this method in the preliminary tax calculation. Check all the entries, and if anything is missing, make corrections as appropriate.

If acquisition details are missing, you should look up the information on the documentation you received from the bank, for example. If you cannot find the details, you can, as a minimum, fill in the year when you bought the securities. The year has an impact on the size of the deemed acquisition cost. To fill in the year, enter it in the Acquisition date field as 1 January. For example, you can simply enter 1 January 1998 and leave the other fields blank.

Details on securities trading as a CSV file

You can also view your securities trading in a table-format CSV file. You can access the file from the start page of the pre-completed tax return:

- In the Individual income tax section, click the link Check your pre-completed tax return.

- Click the link Open details on securities trading as a CSV file.

- The table that opens shows your securities trading saved in the Tax Administration’s records.

Please note that you cannot edit or send data via the table. You can correct details only in the Profit from selling securities section on the tax return. The corrected data will be updated to the table.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your transfers of property. If additions and corrections are necessary, click the Open specification button. This will open a specification on your securities trading. Click the name of the security that contains incomplete information in order to add the missing details.

Alternatively, you can enclose the bank’s specification on your securities trading as an attachment file. If you provide such an attachment, add up the selling prices for all securities you have sold during the tax year and report the gains and losses separately.

- If no transfer information is pre-completed, go to the Other income section and report the information there. Select Yes in the section Profits from selling securities and click the Open specification button.

- Select whether you want to give details on the securities in the specification or as an attachment:

A) I will give the details on the security in the specification

- Click the Add new transfer button

- Select the type of the transfer, i.e. whether the transfer concerns securities or capital.

- Then fill in the required details.

- Finally, click OK.

B) I am submitting details on the securities as an attachment

- First, attach a file you have received from a bank, for example, by clicking the Add file button. Select Attachment regarding sales of securities as the type of the attachment and write a description describing the attachment. You can add multiple attachments.

- Also fill in the fields in the Value of transfers section. Add up the selling prices for all the securities you have sold during the tax year. Also report capital gains and capital losses. Make sure that the details in the attachment match the total amounts entered in the fields.

If you owned bankrupt-company shares, you need to write off the loss caused by the bankruptcy. To receive the tax deduction, do this:

- Click the Open specification button under Transfers of securities, year 2023. Your purchase transactions related to the bankrupt company will appear.

- Click each one of the links that contain names of that company’s shares.

- Because of the bankruptcy, the pre-filled information shows “€0” as their selling price. Check the pre-filled purchase prices and expenses related to the purchases of shares. If everything is correct, click OK. After this, the system will transfer the loss caused by your bankrupt-company stockholding to the tax calculation. If you had bought the shares in several batches, remember to check the pre-filled information on all of them, purchase by purchase.

- If nothing appears on your tax return regarding your shareholding in the bankrupt company, you must enter your shares’ purchase price, the expenses connected to the purchase, and the selling price (€0) into the appropriate fields in MyTax.

Further information

- Read more about the deemed acquisition cost and the taxation of capital gains from the sale of securities

- Read more about taxes on investments

How to file on paper

If you report profits or losses incurred from the sales of securities in Finland and other countries on a paper form, use Form 9A. Also use Form 9A to report any sales carried out through a remote intermediary in a foreign country.

However, Form 16B must be used when reporting other capital income resulting from transactions carried out through a remote intermediary.

This section contains the following:

- dividends from listed companies

- dividends from non-listed companies

- dividends paid out in some other form than money (dividends in natura)

- refunds of capital from listed companies, taxed as dividend income

- profit surplus from a cooperative.

The Tax Administration usually receives the information on receipts of dividends from banks and other intermediaries in Finland and other countries. In the same way, the annual information returns that the Tax Administration has received from unlisted companies and cooperatives have provided the pre-completed dividend and surplus information. Check all the entries, and if anything is missing, make corrections as appropriate. Read more about the taxation of dividends.

Go to the Foreign income section to give details on any receipts of dividend income from sources in foreign countries.

If you are a shareholder-entrepreneur or a majority shareholder

If you are a shareholder-entrepreneur and you have borrowed money from your company, report the amount of shareholder loan in the company’s balance sheet at the end of the accounting period that ended during the year before the year that dividend payment commenced.

Example: You have taken out €10,000 in shareholder loans from the company during the tax year 2022. The company’s accounting period ended on 31 December 2022, and the loan in full was not repaid. The company will distribute dividends in 2023. Indicate the amount of the remaining loan at 31 December 2022, i.e. €10,000.

If you are a majority shareholder and you have used a residential property belonging to the dividend paying company, report the residential property’s value in accordance with the previous year’s calculation of company net worth (the property’s book value in accounting or the taxable value, which is higher).

Enter the value of the residential property only if you own more than 30% of company shares or votes. You are treated as being a majority shareholder also if the ownership interest or holding of votes exceeds 50% when your personally owned shares are added to your family members’ shares.

If you are a shareholder-entrepreneur and you are paid dividends from a company, which is not stock-exchange listed, the mathematical tax value of one share in this company will determine the division between taxable capital income and taxable earnings. If the company was established recently i.e. its shares are new, the mathematical value can be replaced by the subscription price of one share. If you prefer that your taxes on the dividends are assessed based on the subscription price instead of the mathematical value, write up a free-text document to indicate this preference and send the document to the local tax office by post.

For more information, see the Tax Administration’s detailed guide ”Calculating comparison values for one share of a non-listed company” — Julkisesti noteeraamattoman osakeyhtiön osakkeen matemaattisen arvon ja vertailuarvon laskeminen (available in Finnish and Swedish only) (chapters 5.1 “New company” – Uusi yhtiö and 5.2 “New corporate shares” – Uudet osakkeet).

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration concerning your dividends. To make corrections, select the link with the name of the company that paid you dividends. Edit the necessary details. If only some of the dividends and surplus you received are showing, click Add new dividend income to fill in the missing details.

If no details of dividend income or surplus is pre-completed, move on to the Other income stage. Select Yes in the section Dividend income and then click the Add new dividend income button. Select whether you received dividends from listed companies or unlisted companies and report the required details.

How to file on paper

If you provide information relating to dividends on a paper form, use the correct form:

- Dividends and surplus from cooperatives in Finland: Form 50B – Capital income and deductions

- Dividends received from sources outside Finland, and paid foreign tax, if any: Form 16B – Statement on foreign income (capital income).

In addition, complete and submit Form 13 – Account of shareholder loans and distribution of earned and capital income for dividends, if you are

- a majority shareholder and you have used a residential property belonging to the dividend paying company, or you have borrowed money from the company

- a shareholder-entrepreneur and you have borrowed money from your company.

This section includes:

- income in the form of revenues from life insurance contracts, either investment-based or savings-based (including a “shell” contract)

- interest income from private lending

- exchange rate gains

- profits from selling timber if the trees were felled on a plot of land e.g. at a summer cottage.

- Note that you must report profits from selling timber from a plot of land even if the information is pre-filled in the forestry specifications.

- Do not subtract the amount that the timber buyer withheld for taxation. The Tax Administration will give you credit for the amount withheld, according to the annual information return received from the timber buyer.

- You can report the tax-deductible expenses caused by the felling of trees under Other deductions — Other deductions from capital income.

- revenue from the sale of soil

- income from the mining of virtual currency, taxed as capital income (the proof-of-stake protocol).

The Tax Administration usually receives information on capital income from banks, other intermediaries of securities, and from other payors. Check the information and make additions as necessary.

If you received capital income from sources in foreign countries, report that income in the Foreign income section.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your other capital income. If you make corrections, select the link with the name of the capital income payor. Edit the necessary details. If only some of your receipts of capital income are showing, click the Add new capital income button to fill in the missing details.

If no Other capital income section is found pre-completed, go to the Other income stage. Select Yes for Other capital income and then click Add new capital income and fill in the missing details.

How to file on paper

Select the correct form:

- Capital income from sources in Finland: Form 50B – Capital income and deductions

- Capital income from sources outside Finland, and paid foreign tax, if any: Form 16B – Statement on foreign income (capital income).

This section is for the interest income you have received from Finnish payors, including:

- profit paid to an investment fund

- interest paid on bonds or debentures

- paid after market bonus.

However, if you have received interest on an ordinary bank account balance or other interest subject to tax at source, you do not need to report them.

The Tax Administration receives third-party information on almost all interest payments to individual taxpayers and on the taxes withheld on the amounts. Check the information and make additions as necessary.

If you make corrections, report the type and amount of interest income you have received during the entire year and the amounts withheld from it. Do not enter the interest income on which tax at source has already been collected (30%).

If you report interest income that you received from a foreign source, see further guidance for filing in section Foreign income.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of interest income. If you make corrections, select the link with the name of the interest income payor. Edit the necessary details. If only some of your receipts of interest income are showing, click Add new interest income to fill in the missing details.

If no interest income is pre-completed, go to the Other income stage. Select Yes for Interest income and then click the Add new interest income button.

How to file on paper

Select the correct form:

- Interest income from Finland: Form 50B – Capital income and deductions

- Interest income from a source outside of Finland: Form 16B – Statement on foreign income (capital income).

This section is for the profit or loss from your equity savings account if you have withdrawn money from the equity savings account during the tax year. In general, the Tax Administration receives this information from the bank or other service provider. Check the information and make additions as necessary.

How to file in MyTax

The Pre-completed income and deductions stage contains details on your equity savings account, including the profit or loss relating to it. If you make corrections, select the link with the payor’s name. Edit the necessary details.

If no equity savings account profits or losses are found under the pre-completed details, move on to the Other income stage. Select Yes for Profit or loss from an equity savings account, and then click Add new detail.

Further information

How to file on paper

To give details on your equity savings account’s profits or losses on paper, submit Form 50B – Capital income and deductions.

Foreign income

This section lists your foreign earned income. This income includes:

- pensions

- wages and fees

- other earned income such as trade income, pay or fee received by an athlete or artist, scholarships, grants, royalties, and fees relating to Board membership.

The Tax Administration receives information on some items of income directly from the source country of the income; this information is pre-completed on the tax return. Typically, the pre-completed details include pensions received from Sweden, for example. Check the information and make additions as necessary.

How to file in MyTax

The Pre-completed income and deductions stage contains the information on your foreign income that has been available to the Tax Administration. If you make corrections, select the link with the payor’s name. Edit the necessary details. If only some of the income you received from abroad, fill in the missing details.

If no income from foreign sources is pre-completed, fill in the details in the Other income stage. Select Yes at Foreign income. After this, click Open specification under “Foreign earned income in 2023" and report the required information.

Further information

- Further information concerning different types of pensions as shown on the income tax return

- Read about the tax treatment of income from a source outside Finland

How to file on paper

Select the correct form:

- foreign-sourced earned income: Form 16A

- wages paid by a foreign employer for work done in Finland:

Form 50A (Earned income and deductions).

This section lists your foreign capital income. This income includes:

- dividend income

- rental income or losses from a rental operation

- capital gains and capital losses, as well as the number of tax-exempt transfers of assets

- other capital income, such as

- interest income

- income from life insurance contracts, either investment-based or savings-based (including a “shell” contract), with insurers outside Finland.

The Tax Administration receives information on some items of income directly from the source country of the income; this information is pre-completed on the tax return. Typically, these pre-completed details include pensions received from Sweden, for example, or income in the form of dividends from foreign payors. Check the information and make additions as necessary.

How to file in MyTax

The Pre-completed income and deductions stage contains the information on your foreign income that has been available to the Tax Administration. If you make corrections, select the link with the payor’s name. Edit the necessary details. If only some of the income you received is showing, click Add new foreign capital income to fill in the missing details.

If no income from foreign sources is pre-completed, fill in the details in the Other income stage. Select Yes at Foreign income. After this, click Open specification under “Foreign capital income in 2023” and report the required information.

Further information

How to file on paper

Use the form 16B Statement on foreign income (capital income).

Other income

Income related to activities for the production of income include

- freelancer income or family daycare provider’s income (for example, if you are a private family daycare provider with a registration in the prepayment register)

- income in the form of tips

- fees you have received for giving private tuition

- income from dog breeding, e.g. selling puppies or using a dog for breeding purposes, if you are breeding dogs for an income-generating purpose.

This section is not for reporting

- income related to wage income

- income you have made as a self-employed individual.

You are required to report the earned income from income-generating activities that is not shown on your pre-completed tax return.

In addition, you should report all your expenses related to the income-generating activities – this also includes the expenses that are directly related to the income already showing on your pre-completed tax return. Examples of these expenses include:

- materials and supplies

- tools and depreciation relating to them

- workspace deduction.

How to file in MyTax

Report the income from income-generating activities and the expenses relating to those activities in the Production of income section of the Other income stage. Report your earned income in the section Income from income-generating activities in 2023 and the related expenses under Expenses for income-generating activities in 2023.

Also report your travel expenses that are related to the production of income and any increased living expenses due to temporary business trips in their own sections. If you make depreciations on work tools/equipment you have bought, click the Add new depreciation button and fill in the required details.

Further information

- Read more about activities for the production of income (detailed guidance in Finnish and Swedish, link to Finnish)

- Read more about expenses related to the production of income

How to file on paper

If you submit the information on your income and expenses on paper, complete Form 11 – Activities for the production of income.

This section contains the following details:

- Grants, scholarships and awards for merit – including taxable and tax-exempt amounts.

- The expenses that have arisen from your studies, research or other activities for which you have received taxable grants. Deductible expenses include workspace expenses, equipment costs and travel expenses relating to the grants. Itemise the expenses based on whether they relate to taxable or tax-exempt grants.

Your grants are pre-completed on your tax return as reported by the payor. Both the tax-exempt and taxable grants are pre-completed on the tax return. Check the information and make any necessary corrections.

Grants paid to a work group

If the grant was awarded to a group of people, it is usually only shown on the pre-completed tax return of the person who applied for the grant. In these circumstances, you should only report your own share of the grant in MyTax or on the paper form. In the same way, only report the expenses that relate to your share of the grant. The other members of the group will submit their respective tax returns to inform the Tax Administration of their income and expenses.

Awards for merit

If given to you in recognition of academic, artistic or non-profit activities, an award you receive is exempted from tax fully, starting 2023, on the condition that the party giving it to you is an “independent grantor”. This means that your employer, etc. cannot be seen as a grantor of tax-free awards for merit. In comparison with other grants, an award for merit is different because it is given afterwards, whereas scholarships and other grants are normally given beforehand.

Receiving a tax-exempt award for merit is no longer included in the count of grant income and received scholarships, so it no longer has an impact on the threshold of taxes.

Are the prices paid for tools deductible at once, or do I need to calculate depreciation?

If you bought tools or equipment and the price was below €1,200 you can claim the purchase price in full during the tax year when you bought it. Enter it under deductible expenses, line Tools.

If you paid more than €1,200 for tools and equipment and their useful life is longer than three years, your deductions need to be based on annual depreciation expenses. Allowable depreciation for year 1 is max. 25% of purchase price, for year 2, year 3, etc. it will be max. 25% of the remaining purchase price at the end of the previous year.

Read more about depreciation expenses.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of grants. If you make corrections, select the link with the payor’s name. Edit the necessary details. Go to the line Other details concerning the grant to specify the research group that the grant was given to, the grant’s exemption from taxes, the grant’s award-for-merit designation.

If only some of the grant income you have received is showing, click the Add new grant button to fill in the missing details.

In the same way, fill in the expenses related to the grants. Deductible expenses include:

-

Workspace deduction

-

Tools/equipment

-

Travel expenses relating to grants

-

Increase in your living expenses due to work trips

-

Depreciation expenses of the tools or equipment

Itemise the expenses based on whether they relate to taxable or tax-exempt grants. Click Open specification to report your expenses.

If no income in the form of grants is pre-completed, fill in the details in the Other income stage. Select Yes in the section Grants and then click Add new grant. Enter the amount of grants you have received from the same payor during the entire year, as well as other required details. Also remember to report the expenses related to the grants.

If you have received grants from multiple parties, first enter the details on one of the payors and click OK. Then click Add new grant.

Further information

- See which grants are taxable and which are tax-exempt

- See examples about how to inform the Tax Administration of an academic grant received by a work group

- Read more about the requirements of tax-exemption of awards and grants

How to file on paper

If you submit the information on paper, fill out Form 10 Grants.

This section shows how much you have borrowed between 1 January and 31 December from a company where you are a shareholder. Only the amount that you have not repaid by 31 December is subject to taxation as a shareholder loan.

A shareholder loan is part of your taxable capital income if you, alone or with a family member, own at least 10% of the company’s shares, or have a corresponding voting interest in the company.

The annual information return that limited liability companies are required to send to the Tax Administration has been the source of the pre-filled amount on your tax return. It is required of all limited liability companies to send information on the amounts borrowed and the amounts repaid by company shareholders. This rule concerns the shareholders who are natural persons. These loans are taxed as capital income. Check the information and make additions as necessary. If you hold shares in a foreign limited liability company and you have borrowed money from it or paid a loan back to it, please fill in the information for this section yourself.

How to file in MyTax

The Pre-completed income and deductions stage contains the information made available to the Tax Administration on your shareholder loans. To make corrections, select a loan and edit the details.

If no shareholder loans are found under the pre-completed details, fill in the details in the Other income stage.

Further information

- Read about the tax treatment of shareholder loans (detailed guidance in Finnish and Swedish)

How to file on paper

If you report details on shareholder loans on a paper form, use Form 13 – Account of shareholder loans and distribution of earned and capital income for dividends.

This section is for any occasionally earned income, which is not based on an employment contract and not classified as trade income. Examples of other earned income are:

- financial support or grants received for a recreational activity or for hobbies

- finder’s reward or competition award

- income from the mining of virtual currency (Proof-of-work protocol)

- occasional income from dog breeding, e.g. selling puppies or using a dog for breeding purposes as a hobby.

Report every item of income separately. Write a brief description of the income items. Also indicate the sum total of income received for the entire year (1 January to 31 December). Enter the total gross amount of income, i.e. do not subtract any taxes or charges that have been collected.

If you have received money for an activity that you have repeated many times during the year, give details on the income and deductible expenses in the Production of income section instead.

Did you use a platform, app or website to offer services to customers? The Tax Administration receives information concerning the income paid to you through digital platforms both in Finland and abroad. The Tax Administration requires that you report all this income, and we also exercise control. If you sold personal services during the tax year (such as beautician’s services, house cleaning work, other personal service) and you connected with your customers over a digital platform, fill in the tax return giving details on your income and related expenses.

How to file in MyTax

To give details on your other earned income, go to the section Other earned income in the Other income stage.

To report any related expenses for the production of income, go to Other deductions. Select Yes for Expenses for the production of income, and then enter the details in the section Expenses for the production of other income than wage income.

Further information

How to file on paper

To report your other earned income on paper, submit Form 50A – Earned income and deductions.

This section contains the amounts of profit-surplus distributions you have received from a cooperative, including interest on cooperative capital.

In general, the Tax Administration receives information on paid-out profit surplus directly from cooperatives on the annual information returns they submit. Check the details, and if anything is missing, make corrections as appropriate.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your receipts of surplus from cooperatives. If you make corrections, select the link with the payor’s name. Edit the necessary details. If only some of the surplus you have received is showing, select the Add new surplus button to fill in the missing details.

If no surplus income is pre-completed, move on the Other income stage. Select Yes for Surplus from cooperatives and then click the Add new surplus button.

How to file on paper

To report your receipts of surplus from Finnish cooperatives on paper, submit Form 50B – Capital income and deductions.

Tax deductions

Typical deductions and credits

You can claim the expenses of your daily commute and other travel expenses related to your work.

Deductible expenses include:

- the ordinary commuting expenses, between home and work

- expenses for going home for the weekend if you work far away from where you live

- the commute between your permanent residence (home) and a secondary place of work

- certain trips, mostly in specific fields of work such as construction, to a special place where work is done

If you have informed the Tax Administration of your work-related travel expenses during the year, when you requested a tax card or prepayment, etc., there will be a pre-filled deduction on your tax return accordingly. After you check the pre-filled amounts, make any necessary corrections and additions. Add any deductible commuting/travel that you have not yet claimed.

- If you do not reach the threshold of €750 in commuting expenses between home and work, there is no need to submit the information. For the 2023 tax year, this category of expenses has a 750-euro threshold of deductibility.

- You exceed the threshold if you spent more than €750 on commuting and travel, so you should declare the entire amount of your expenses. Do not subtract the 750-euro threshold from the total expenses.

- For your tax year’s 2023 assessment, you can no longer claim any deductions for face masks worn on mass transport.

How to file in MyTax

The Pre-completed income and deductions stage contains the information on your travel expenses that has been available to the Tax Administration on your expenses. If any corrections and additions must be made, choose the means of transportation first (public transport, other than public transport, or a combination of both), then make the required changes to your tax return. Make the necessary changes. If just a part of the year’s expense is showing, click the Add new travel expense button to fill in the amounts that are missing.

If no commuting/travel expenses appear as your pre-filled deductible expenses, enter data in the Other deductions stage as appropriate. Select Travel expenses first, then click the Add new travel expense button.

Please note that you have to itemise by category of travel; for example, a specific line is reserved for the daily commute between home and work.

Further information

How to file on paper

Use the right form:

- the commute from home to work and back: Form 1A

- expenses for going home for the weekend if you work far away from where you live: Form 1B

- expenses for commuting between your permanent residence (home) and a secondary place of work: Form 1C

- expenses for temporary commuting to a special place where work is done: Form 1D

To get the tax credit, you must indicate the expenses paid during the tax year for relevant work assignments in the household. Possible expenses include:

- Renovations i.e. home improvement

- Cleaning and other household work

- Nursing and caregiving

You can receive the credit if you have bought the work as a service provided by a prepayment-registered company, or if you have hired someone as your employee to do the work.

If you informed the Tax Administration of your claim during the tax year (when you requested a tax card or prepayment), your pre-completed tax return may already refer to a credit for household expenses. The credit’s details are also pre-completed if you have agreed with the company that performed the work that it send the details and amounts to the Tax Administration on your behalf. Please check the pre-completed information carefully, and make any necessary corrections and additions as needed.

If you employed someone and you are a user of the Palkka.fi website that handles payroll accounting, the household expense information is automatically transferred to the pre-completed tax return.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your credit for household expenses. If it is necessary to make corrections or to claim less credit for household expenses, select the company’s name or your employee’s name first. You can edit the entries now. If just a part of your household expenses and related information for the tax credit is showing, click the Add a new expense button to add the amounts that are missing.

If no information about the credit appears among your pre-filled deductions, enter data in the Other deductions stage as appropriate. Select Yes for Credit for household expenses first, then click the Add a new expense button.

How to file the tax credit for household expenses in MyTax

Further information

Read more about the tax credit for household expences

How to file on paper

Use the right form:

Another tax credit available for the tax year 2023 is a credit given to those who had to pay exceptionally high expenses for electricity in their home. Only the expenses for January, February, March and April 2023 are accepted.

If energy charges and fixed basic charges related to electricity consumption in your permanent home between 1 January and 30 April 2023 exceed €2,000 you can fill in the amounts paid.

- If you do so, make sure not to include electricity for December 2022 even if the due date of the December 2022 invoice were in January 2023.

- Include electricity for April 2023 even if the due date for the invoice might be in May 2023.

- Do not include electricity transmission and other comparable extra costs. For these costs, no tax credit for electricity can be granted.

If you informed the Tax Administration of your claim during the tax year (when you requested a tax card or prepayment), your pre-completed tax return may already show this credit. Check the expenses you actually paid for electricity, and make corrections as necessary.

How to file in MyTax

The Pre-completed income and deductions stage, under Tax credit for household expenses, contains the information available so far to the Tax Administration concerning your expenses. If it is necessary to make corrections or to claim less credit for electricity, click Open specification. You can edit the entries now. If you only see other expenses, having to do with your other tax credits related to the household, not related to electricity, click the Add electricity costs button.

If no information about the tax credit for electricity and the tax credit for household expenses appears among your pre-filled deductions, please move on to the Other deductions stage. Select Yes for Credit for household expenses first, then click the Add electricity costs button.

How to claim the credit in MyTax

Further information

Read more about the tax credit for electricity

How to file on paper

If you inform the Tax Administration of your electricity expenses on paper in order to claim the credit, complete Form 14D Tax credit for electricity – household expenses related to electricity costs 2023.

If you are a member of a trade union or an unemployment fund, you can receive a deduction relating to:

- the membership fees that you paid, or

- the unemployment fund’s fees

In most cases, the Tax Administration receives information directly from trade unions and unemployment funds, including lists of fees paid to them. After you check the pre-filled amounts, make any necessary corrections and additions.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on membership fees. To make any corrections, first select the name of the trade union or unemployment fund. Now, you can edit the entries if necessary. If just a part of the fees you paid is showing, click the Add new membership fee button to make corrections.

If no paid fees appear among your pre-filled deductions, enter data in the Other deductions stage as appropriate. Select Yes for Membership fees for labour market organisations first, then click the Add new membership fee button.

You need to fill in the name of the trade union/organisation or unemployment fund and its Business ID. If you do not know the Business ID, contact the union/organisation/fund that you pay the fees to. Enter the amount you paid during the year, or correct the pre-filled amount if needed.

How to file on paper

To claim the deduction on paper, submit Form 50A – Earned income and deductions.

You can claim deductions for some of the expenses related to your income from employment. The expenses in this category include:

- the expense you must pay for a workspace

- the personal tools you may have

- the expenses for books relating to your occupation or profession

- the training expenses you pay

- the increased living expenses due to work trips

- the shop steward’s fees you pay

In addition, you can claim deductions for expenses that are related to other income than your wage income i.e. other activities than your employment, including:

- expenses for the production of other work income, typically related to nonwage compensation, “trade income”. Example: the fees you must pay to an invoicing-service company

- expenses for the production of income relating to benefits and other earned income

If you receive income from an activity that is recreational or a hobby, you cannot claim deductions higher than up to the amount of received income only.

This section is only for employment-related expenses – do not enter your expenses relating to academic grants, to other grant income, your deductions for a second home for work, expenses related to your capital income. Claim the above deductions under the tax return’s sections that are intended for them.

Note: there is a 750-euro threshold of deductibility

If you do not reach the threshold of €750 in expenses for the production of income, there is no need to submit the information. You get the standard deduction, €750, for the production of income automatically.

If you spent more than €750 on the production of your income, on acquiring income, on maintaining income, etc., you exceed the threshold. In that case, you should indicate the entire amount of your expenses. Do not subtract the 750-euro threshold from the total expenses.

If you have given the Tax Administration the amounts of your expenses during the year, when you requested a tax card or prepayment, etc., your pre-completed tax return shows your deduction. After you check the pre-filled amounts, make any necessary corrections and additions.

You should add the expenses for production of income that you have not yet informed the Tax Administration of.

How to file in MyTax

The Pre-completed income and deductions stage contains the information that has been available to the Tax Administration on your expenses for the production of income. If it is necessary to make corrections or to claim less expenses for the production of income, select Open specification to make an itemisation appear. Now you can edit the entries. If just a part of your expenses is showing, fill in the amounts that are missing.

If no expenses for the production of income appear among your pre-filled deductible expenses, enter data in the Other deductions stage as appropriate. Select Yes for Expenses for the production of income. Then click Open specification. Please note that you have to keep the expenses relating to your wage income separate from the expenses that are relevant to your other types of income that are not wages from employment.

How to file expenses for the production of income in MyTax

Further information

- Read about the types of expenses that may qualify for the deduction for the production of income

- Read more: working from home — tax-deductible expenses

How to file on paper

To claim the deduction on paper, submit Form 50A – Earned income and deductions.

The following interest payments are tax-deductible:

- Interest expenses on a loan you have taken in order to gain or produce income, to invest in corporate stocks, securities or a residential apartment, etc. If you have taken such a loan, you can deduct the year’s interest payments in full.

- Part of the interest expenses on a loan you have had to take when you had made a commitment to repay someone else’s debt, in order to make good on the commitment.

As of the 2023 tax year, no home-loan interest payments, including first-time homebuyer’s home loans, are tax-deductible. In the same way, no interest expenses on other debt such as consumer credit can be deducted.

Please check whether the loan’s purpose of use is pre-filled right